Why is the Conejo Valley and Surrounding Areas Homes for Sale Inventory so Low?

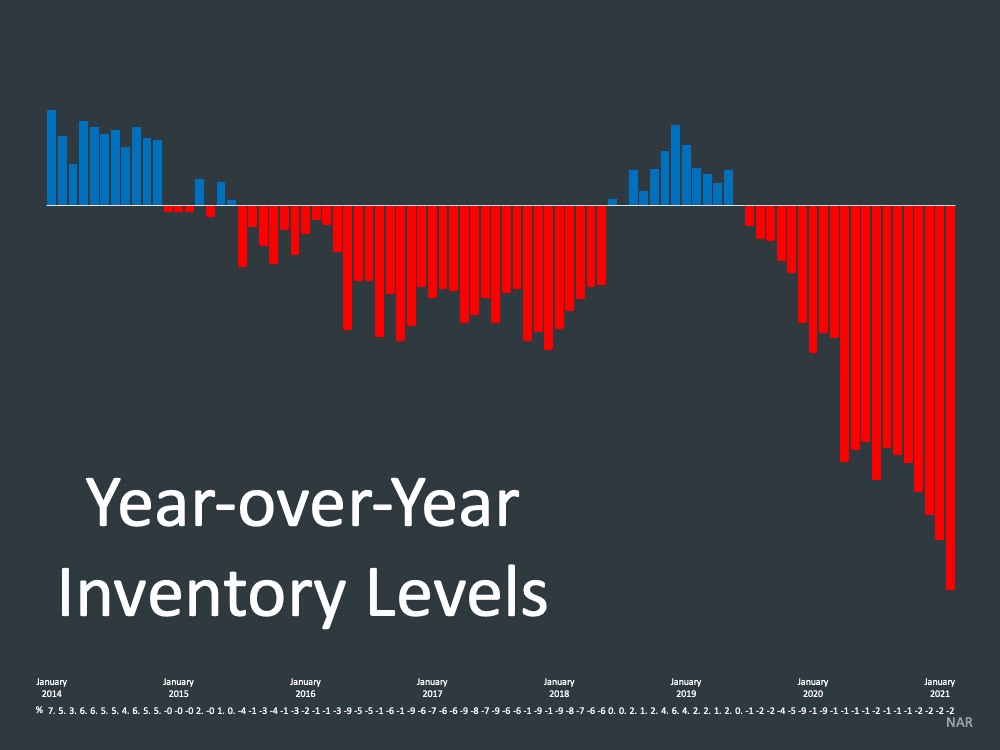

We are facing a serious housing shortage, with the lowest inventory of homes for sale in over 39 years. Total housing inventory is down 52% and purchases up 32%, creating an extremely competitive home-buying market.

This is great news for sellers. Homes are selling at record prices in record time with multiple offers. This is not just a seller’s market. It has been called a super seller’s market. But will it continue through the year?

Most economists think so. Real estate continues to be the shining star during this global pandemic that devastated the economy.

People were shuttered in their homes during most of 2020 and into 2021. They are relegated to working from home and homeschooling in the same apartment, condo, or small home that served them well before COVID-19. Those four walls were quickly closing in around them.

Mornings no longer involved packing up kids, dropping them off at school, and driving to an office to work. Their time together used to be a few hours in the morning and then from dinner to bedtime. Now it’s 24/7.

They needed bigger homes. They needed home offices, an extra bedroom, a family room, and a yard for kids to burn off energy.

No longer tied to driving to a physical office, their working-from-home routine allowed them the freedom to move to less expensive areas. Communities like the Conejo Valley and surrounding areas were the chosen destination for many downtown L.A. and Westside homebuyers who fled to find a better environment. Some left the state for even more affordable housing.

Once everyone came to the sober realization that COVID-19 really was a global pandemic and was not going to end anytime too soon, the demand for housing rose rapidly

The requirements for a home are much different during the pandemic than in the past. Without the ability to freely roam about town to shop. dine out at restaurants, visit friends, go to concerts and movies, or take a vacation, “home” became a round-the-clock work-learn-exercise-entertainment center that had to simultaneously provide some semblance of individual privacy for all occupants. That required more space.

People are driven to seek homes with more amenities. Features that they used to view as luxuries are now deemed essential. Private, spacious yards, swimming pools, home gyms, extra bedrooms, additional office space, and attached 2 or 3-car garages are at the top of the list.

But those homes are hard to come by because sellers held back on putting their properties on the market when the pandemic started. Fears of strangers roaming through their homes during the time of coronavirus kept homes off the market. The rate of purchasing quickly began to exceed the rate at which homes came on the market.

The other factor that is straining the housing market might surprise you. Millennials have entered the housing market in unprecedented numbers. For years, real estate economists have questioned why this large demographic group has resisted home buying. A 2019 Millennial Homeownership Report by Apartmentlist.com reported that many Millennials planned on renting “forever,” and this number grew even higher in major metropolitan areas.

At about the same time COVID hit, Millennials started to turn 40. They now make up the largest group of homebuyers in America. Believe it or not, Millennials make up 38% of the home buying pool. Not only are they buying homes, but many are buying million-dollar starter homes.

The pandemic, coupled with historically low-interest rates, has incentivized hard-working Millennials who have rented for years to enter the housing market.

So what is the Recipe for a Housing Shortage Crisis?

- Low-Interest Rates

- Sellers holding off from selling due to COVID-19

- Need for more space

- Freedom to live anywhere

- Need to work-teach-entertain at home

- Rise of Home-Buying Millennials

Are We Near a Housing Bubble?

People have referred to the current market as “frothy,” “unsustainable,” and “a bubble.” But many economists, real estate leaders, and banking investors believe that the housing market is expected to continue with its imbalance of high demand and short supply of homes.

However, an adjustment will eventually catch up to the market and turn the market demand. The expectation is that we will experience a “soft landing” where the pace of buyer demand slows and inventory builds, allowing more buyers to purchase without the bidding wars of today.

Two other factors could help increase inventory later this year.

Proposition 19 might stimulate more “Boomers” to sell their homes, and potential home sellers will become less COVID-19 fearful.

Interest rates are expected to remain low but rebound from their lowest points. This could curb some buyers who are waiting on the sideline.

Overall, the housing market will show signs of improvement for buyers. They will have more opportunities to purchase while it remains fairly strong for sellers.

Should You Sell Now?

This is the prime selling season, and the market is fueling it in your favor. If selling a home is in your plans, this is the time to take action.

We have never been proponents of sellers and buyers “timing the market.” That is a very slippery slope. If the market turns downward, it happens rapidly. It takes longer to sell a home, and homeowners lose money as they “chase the market” to attract buyers. If they sell before the market turns, they feel they sold too early.

Few homeowners can claim they “sold at the top of the market.” If they were that successful, it was most often luck and not shrewd planning. But in our opinion, it is better to err on the side of selling before the market turns and leave a little money on the table rather than wait and risk the chance of getting caught in a downward spiral of a declining market. Historical real estate crashes trigger rapidly and if you miss the peak, the opportunity to escape the spiral will have passed.

While many authors will cite “unsustainable rising housing prices” as the reason for the crashes, that is an incomplete and inaccurate statement. Public panic in response to news events triggers real estate crashes. One morning you wake up, and news of a stock market crash, mortgage banking fraud, or massive job losses initiates a loss of consumer confidence and the resulting real estate crash.

Most real estate crashes, as well as real estate down-turns called “market adjustments,” were triggered by consumer panic in response to stock market crashes. However, the two most recent crashes, the 1987-1995 Savings and Loan Crisis and the Great Recession (crash of 2007-09), were further complicated by the collapse of the banking and lending institutions.

Property is unlike a stock that you can sell with a single call or click of a button in response to daily events. It takes preparation, and time to market the property, receive offers, and then hope that your buyer stays in the game throughout the term of the escrow. If you are on the market during a “panic event” the flowing faucet of buyers is turned off nearly immediately while they wait to see what is going to happen. And what happens is that real estate sales plummet before a home seller can act.

We counsel homeowners and homebuyers to sell and buy according to their personal needs rather than “timing” the market.

If you require a change in your housing needs, start planning now. We’ve helped clients since 1987 through three major housing booms and two disastrous recessions. We’ve experienced a lot of tricky situations and have the acumen and knowledge to help you through them with great success.

Get the tips for selling for top dollar!

Should you sell now or later? Can you time the market? Let's have a chat to see how we can get you top dollar for your home!