Home Buyers are Competing in a Super Sellers’ Market

The inventory of homes for sale across the country is down 52% but purchases are up 32%, creating an extremely competitive home-buying experience.

A seller’s market is when more buyers are competing for fewer homes. That’s exactly where we are in this Spring 2021 home-buying market.

Buyers are facing multiple offers against numerous other buyers. We have seen listings with five to thirty offers from well-qualified buyers.

For buyers, it’s frustrating and may feel fruitless as you find yourself repeatedly outbid by other buyers. But with the right plan, you can get the house of your dreams.

First, understand the market. Our recent blog of “Real Estate Inventory is the Lowest in Decades,” spells out why and gives hope for buyers in the coming months.

Tips to Compete in a Super Sellers’ Market

Get Fully Approved with a Well-Qualified Local Brick and Mortar Lender.

Preparation, understanding, and patience will get you through this. First and foremost, align yourself with a local, trusted, and experienced mortgage broker with whom you, a friend, or your agent has worked with successfully. This is not the time to rate shop lenders you don’t know!

You need a trusted mortgage broker to watch over every step of your loan. If you want your offer accepted, the listing agent needs to know that you are working with a committed mortgage broker who will keep working hard until it is closed on time. Online brokers or out-of-area lenders could spell trouble in getting your offer accepted. Internet lenders might be fine for a refinance but not for a purchase.

Your lender will provide you with a pre-approval or full approval letter to accompany your offer to the buyer. This letter is the backbone of your offer. Without proper financing, you have no ability to buy. The strength of that letter can help “sell your offer to the buyer and listing agent.

There is a significant difference between pre-approved and fully approved. A pre-approval carries no weight in a seller’s market. It means you called “any” lender and told them basic details of your finances, and they wrote a letter stating that you are loan worthy. They may or may not have even run your credit score. This shows the seller and listing agent that you haven’t done your homework and aren’t as prepared as other potential buyers.

You need to be fully approved, not pre-approved. Full approval means that you met with a lender, completed a full loan application, submitted all income and banking documents, and they input your information through a Fannie Mae/VA/FHA online loan application underwriting center. It generates Conditional Approval that becomes your walking papers to go shopping for a home. Few home buyers go through the full approval process before making offers. But if you do, and you are against other buyers with pre-approval letters only, you are likely to be given a much higher consideration by the sellers and selling agents.

Leave Your Ego at the Door!

When you find the right house, it’s game time! Only one offer can win, and it needs to be you! So, play like a player. This is no time to get insulted or mad, feel like you are being taken advantage of, or take anything personally.

The seller has the upper hand. They have several offers to consider and are looking not only for the best price but the best terms, the best-qualified buyer, and the most committed buyer. The listing agent also consults the seller on what to look for in a winning offer.

So, if you are lucky enough to be one of the buyers to receive a Seller Multiple Counter Offer, be excited that you passed the first screening.

Look at it as an opportunity, and don’t be insulted that they made demands by countering several terms. Sure, we know it stings after you made your best offer to be told you must come back again with the “highest and best price.”

But the winners will be the buyer and agent who responds positively and looks for things they can bring to the table that sweetens their Buyer Counter Offer. You need to show that you are professional, serious, and committed to closing the escrow.

If your ego takes over, you are likely to walk away, only to be left doing the same thing on the next home offer. And the next one. And the next. The market continues to go up. Interest rates rise higher. And eventually, you can no longer afford to buy a home in the neighborhood you are in now considering.

What Else Can You Offer?

Despite what you may think, “price” is not all that the seller is looking for. Of course, you will have to do your best with the price. But we’ve had several client’s offers accepted when they weren’t the best price simply by giving the seller other items of value.

- Offer to pay seller’s closing costs, including escrow, title, and/or HOA transfer fees. Psychologically, this shows you are helping them by making it easier on them. Instead of raising your offer by $5,000 you are lowering their expenses by $5,000. It may turn out to be the same net for the seller looking at another buyer’s slightly higher offer. But your effort may be seen as an olive branch and put your cooperative offer in a favorable position.

- Offer to let the seller stay in possession at no cost for 3o or even 60 days if that is something your agent finds out is important to the seller. This really requires that you leave your ego at the door. It doesn’t settle well with most buyers that they let the seller live in their new house for free while they must pay the mortgage and property taxes for a month or two. But it may just be the tipping point for getting your offer accepted over someone else’s. We have used this negotiation technique several times, and it works! We recently helped a VA Zero Down Payment buyer compete on a property with other offers. They used this strategy, and their offer was accepted!

- Reduce the Buyer Inspection Contingency from the standard 17 days to 10 or 7. That lets the seller know you are ready and willing to hustle to get all inspections out of the way and remove that contingency. The sooner the contingency is removed, the more security it gives the sellers that you will complete the purchase.

- Waive the Appraisal Contingency. This is HUGE. And it may get your offer accepted over others even if it isn’t the highest price. In a market where offers are coming in over the list price, the sellers have a real concern that the highest price may not appraise, and they might favor the buyer who can take this concern away. If you have cash or a large down payment, you can consider removing the appraisal contingency. With a large down payment, you can receive a lower appraisal, and the bank will still make the same loan for you.

Here’s how it works. The lender will loan you X% of the appraised price. Suppose that you are putting 20% down. The lender will then lend you 80% of the appraised value. But if it appraises lower, the lender will only give you a loan of 80% of that amount. If you offer on an $800,000 property, you expect that the lender will lend you 80% of the appraised value, which is $640,000. But if it appraises at $780,000, the lender will only give you 80% of $780,000 or $624,ooo. That’s a $16,000 difference. If you remove your appraisal contingency, you agree in advance to bring more money in as a down payment to cover the difference. This does not mean you are paying $16,000 more for the property. You are just paying more down payment and getting a smaller loan. Your offer would provide the seller with the security that you won’t fall out of escrow over an appraisal issue. This is a big benefit to the seller and could make the difference between the house being yours or another buyer’s.

- Offer an Escalation Clause. Not every buyer or buyer’s agent will think of this. But it can work to get your offer accepted if you are willing to accept the gamble. Essentially, you offer to pay a set amount over the highest offer. For example, “Buyer agrees to pay $1000 over the highest bona fide offer. Proof of highest offer to be provided.” This only works if you really are prepared to go up in price. But it could make you the winning offer.

- Know the comps! In a buyer’s market, analyzing the comparable sale keeps you from paying too much. But this is a super seller’s market that requires a different strategy. It’s not uncommon for a listing agent to list a property “low” to drive a fury of buyers that ramp up the price. Remember that ego thing? Let it go. Don’t think in terms of “paying over list price.” We can’t count the times we’ve heard, “I won’t pay that price!” But someone else does, then they have the home, and you don’t. Then the next listing in that neighborhood is over that sold price! So, look at the listing price vs. the comps. Perhaps a $50,000 over list price isn’t really paying too much.

WARNING! We have seen buyers waive inspection contingencies in order to compete or even being countered by sellers to waive them. We highly advise against waiving this contingency. You need to know what you are buying and to be protected by doing your property inspection and having cancellation rights in the event something really serious is discovered.

Don’t forget that these strategies require you to let your ego go! After all, your goal is to get the house. And in this market, this is what needs to be done to make it happen.

Should I Wait to Buy Until Prices Come Down?

On the surface, this sounds reasonable. Eventually, the market will settle. But should you wait for that time? It sounds like a good deal if you wait to buy when home prices slow down and drift lower in price. But the real factor to think about is affordability. How much is buying the house costing you each month? That is a factor of the purchase price and interest rates.

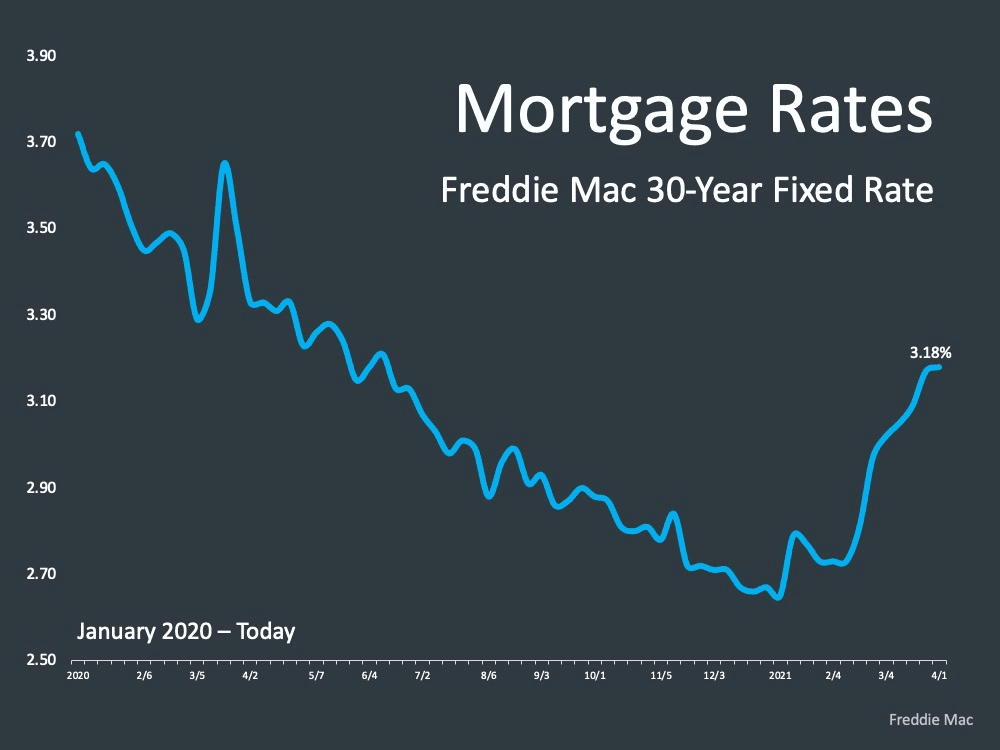

Let’s take a look at an example of how affordability works. Suppose you are considering a house that is listed for $750,000 but might take $780,000 to be the winning offer. With a 20% down you have a loan of $624,000. Your loan interest rate is 2.95% giving a principal and interest payment of $2,627/month. Now suppose you decide to sit on the sidelines another year or two. Maybe the market softens and a house in that neighborhood you wanted is now $740,000. Your loan would be $592,000. How exciting! But wait. Interest rates are starting to rise and will likely continue. Expectations of 4% and higher are not out of the question. So now, your $592,000 loan at 4% is creating a payment of $2,826 or almost $200/month more. That same home will cost you $2,400/year more to own.

Are prices expected to come down? Not soon, according to most economists. Frank Martell, CEO of the housing analytics company CoreLogic, recently stated: “Given the economic outlook, housing remains a bright spot for the foreseeable future.”

Should I Just Wait to Buy a Foreclosure?

Given the pandemic-related job losses and mortgage forbearance programs that are set to expire soon, one would expect a high number of homeowners will be unable to make their payments and be forced into foreclosure. With the foreclosures of the Great Recession still a bad memory in our minds, this seems a possible scenario. But this is 2021. It is not like 2008. Here’s why.

The housing crash of the Great Recession was caused by unreasonable lending risk in a rapidly rising housing market. Homeowners got into homes with little credit requirements and little to no money down. Quite simply, they had no skin in the game. When the market turned and prices slipped, homeowners who had no equity in their homes panicked and walked away. Eventually, lenders established short sale guidelines that encouraged more responsible homebuyers to take advantage of the escape from their “underwater” homes because they had no equity in their homes. That put even more homes on the market.

This is 2021. Nearly 40% of homeowners in America own their homes mortgage-free. The percentage of homeowners with equity is the highest in over fifty years.

Most homeowners have already worked out forbearance plans with their lenders and will come out of the pandemic by still owning their homes.

Some won’t. But the majority of those homeowners who cannot afford to keep their homes have significant equity. So, they won’t walk away. They will likely sell their homes in a strong seller’s market and get the highest possible price for their home.

There won’t be many foreclosure opportunities for buyers in Southern California as a result of the pandemic.

Things Will Get Better for Buyers

If you have been struggling to buy a home, there is encouragement in the coming months.

The inventory of homes for sale will start to improve as sellers become less COVID-19 fearful. People will become more comfortable moving about as vaccinations continue, COVID-19 cases decrease, and stay-at-home restrictions are lifted.

Home inventory is also expected due improve later this year due to the start of Proposition 19, which went into effect on April 1. 2021. Proposition 19 is expected to stimulate more “Boomers” to sell their homes, freeing up more properties for buyers to purchase.

Finally, the pool of buyers is showing signs of slowing. Many of them have made their move, especially cash buyers who have been beating out even the best-qualified buyers with loans.

There was an abundance of cash buyers who were in escrow last winter before Covid-19 halted all selling activity. Their buyers worked hard to close escrow, and the sellers banked the money and rented until the housing market improved. They were back in full force this winter, and most have made their purchases by now.

If you want to know more about buying in this market and how our proven strategies have helped our clients compete in this market, give us a call, text, or email. We’ll get right back to you!

Want more tips about buying in this market?

A quick chat might make the difference between owning a home and losing out on another! Get the tips that help our buyers compete successfully!